The Crossover Enterprises Were Told Would Never Happen

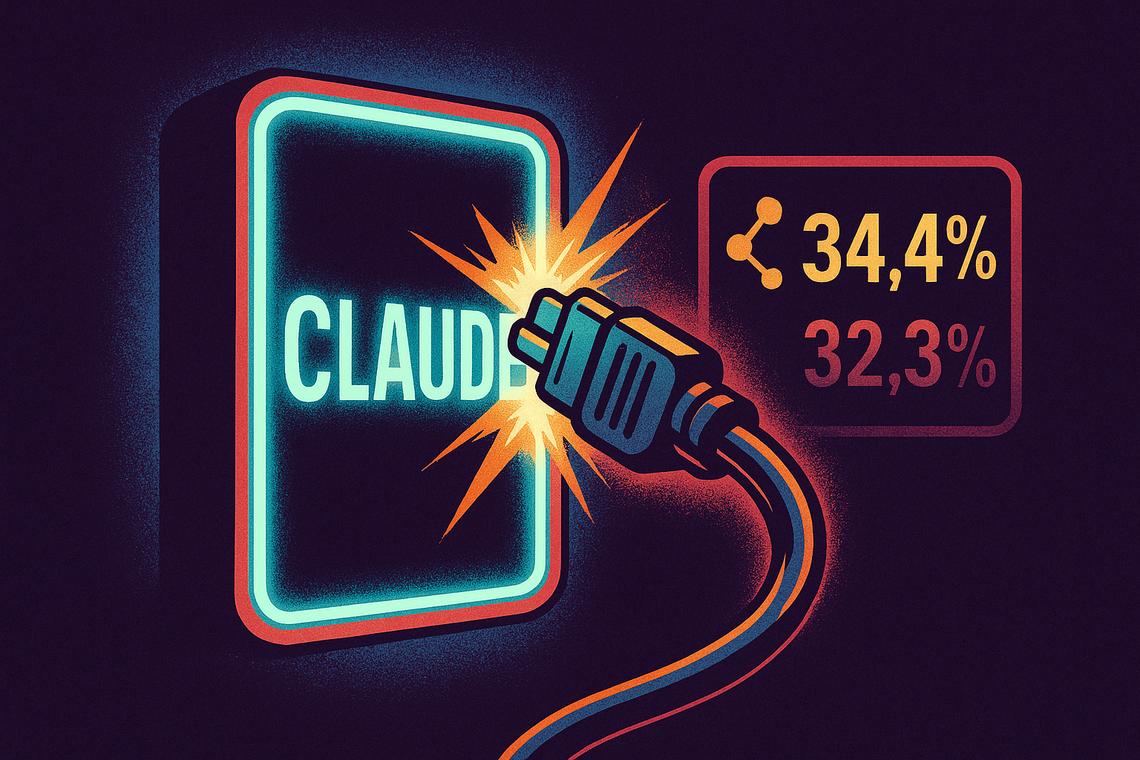

For two years the working assumption in nearly every enterprise AI strategy deck was simple: OpenAI is the default, and everyone else is trying to catch up. That assumption has now broken. The Ramp AI Index, which tracks actual paid spending across more than 50,000 US businesses, recorded Anthropic at 34.4 percent of tracked companies in its May release covering April data, edging past OpenAI at 32.3 percent. It is the first time since the modern AI race began that more American businesses are paying for Claude than for ChatGPT, and the gap is widening rather than closing.

The trajectory matters more than the single data point. Anthropic climbed from 0.03 percent of businesses in June 2023 to 7.94 percent by April 2025, then to 34.44 percent by April 2026. OpenAI peaked near 36.5 percent in mid-2025 and has drifted down since. The June 2026 Ramp update pushes Anthropic to roughly 41 percent of US businesses with paid AI subscriptions against OpenAI's 38 percent. In the span of a year, Anthropic quadrupled its business adoption while OpenAI grew its own by a rounding error.

What the Spending Data Actually Measures

Ramp's index is not a survey of intentions or a count of free sign-ups. It is built from corporate card and bill-pay transactions, which means it captures money that finance teams have actually committed. That distinction is the reason this particular dataset has become a closely watched leading indicator. As Ara Kharazian, Ramp's lead economist, put it: "Anthropic takes the lead following a banner year of month-over-month increases in business adoption." Paid penetration is a harsher test than usage chatter, because it reflects budget decisions that someone has to defend.

We would caution against reading the headline as a clean verdict on model quality. Ramp measures breadth of paying customers, not depth of deployment. A separate IDC survey of more than 1,000 organizations found only 19 percent reporting extensive Claude use, with OpenAI and Google still ahead on how deeply their tools are embedded. The honest reading is that Anthropic has won the widest base of paying business accounts, while the contest over who powers the heaviest, most mission-critical workloads remains genuinely open.

Claude Code Is the Engine

The single biggest driver of the swing is Claude Code, Anthropic's agentic coding tool, which the company describes as the fastest-growing product in its history. Ramp estimates Claude Code now accounts for roughly 4 percent of public GitHub commits, a remarkable figure for a product that did not exist in its current form eighteen months ago. Coding is the wedge: it lands with technical teams who can quantify the productivity gain immediately, then spreads outward into finance, legal, and research workflows where Anthropic's reputation for instruction-following and long-context reliability pays off.

This is the part enterprise leaders should internalize. Anthropic did not win the broad business market with a consumer chatbot or a flashy demo. It won it through a developer tool that produces measurable output, then rode that credibility into adjacent functions. For CIOs evaluating where the durable enterprise value sits, the lesson is that agentic, work-completing tools are converting trials into paid seats faster than general-purpose assistants. The model is becoming a commodity input; the workflow it completes is the product.

Three Threats That Could Erase the Lead

Anthropic's position is real but fragile, and the cracks are already visible in Ramp's own commentary. The first threat is reliability. Customers reported frequent outages, rate limits, and rising dissatisfaction in recent weeks, the kind of operational friction that erodes trust precisely as workloads scale. Anthropic reset usage limits in April and has been scrambling for compute, signing a SpaceX-linked data center deal among others, but capacity has been a recurring constraint rather than a solved problem.

The second threat is cost. A Ramp colleague found that a recent Anthropic model update would triple token costs for any prompt containing an image, and Uber's CTO publicly noted the company had already blown through its 2026 AI budget. The third threat is OpenAI's countermove: a faster product cadence and aggressive enterprise pushes through partners like Cognizant and CGI for its Codex coding agent. Leadership in this market has proven to be a monthly variable, not a moat.

The Multi-Model Reality Sets In

The deeper signal in the Ramp data is not which vendor leads but how quickly leadership now changes hands. OpenAI held a commanding position for two years; Anthropic erased it in roughly twelve months. That velocity should reshape procurement. Single-vendor commitments look increasingly risky when the relative quality, price, and reliability of frontier models can flip within a quarter. The enterprises insulating themselves are the ones building an abstraction layer that lets them route workloads across providers and renegotiate from a position of optionality.

This is also why we keep seeing platform vendors hedge rather than bet. Salesforce, ServiceNow, and Google have all moved to support multiple frontier models inside their stacks rather than marry one. The Ramp crossover is best read not as a coronation of Anthropic but as confirmation that the model layer is contestable and will stay that way. The advantage in 2026 belongs to buyers who treat the frontier labs as interchangeable suppliers competing for their spend, not as strategic partners whose roadmaps they must follow.

What CIOs Should Do With This

The practical takeaway is to treat the Ramp index as a prompt to audit your own exposure rather than as a buy signal. If your organization is concentrated on a single provider, the past year is a vivid reminder of how fast the calculus can change. Pressure-test your contracts for portability, instrument your usage so you can actually compare cost-per-task across models, and pilot a competing provider on a non-critical workload so switching is an exercise you have already rehearsed rather than a fire drill.

It is equally worth watching what Anthropic does with its lead, because both Anthropic and OpenAI are heading toward public markets, with Anthropic reportedly targeting a fourth-quarter listing. A vendor under public-market scrutiny faces new pressure on pricing, margins, and disclosure, all of which feed back into the reliability and cost concerns that already shadow Claude. The crossover is a milestone, but in a market where leadership turns over in months, the more useful question for any CTO is not who is ahead today, but how cheaply you can change your mind tomorrow.