A Market Growing Up

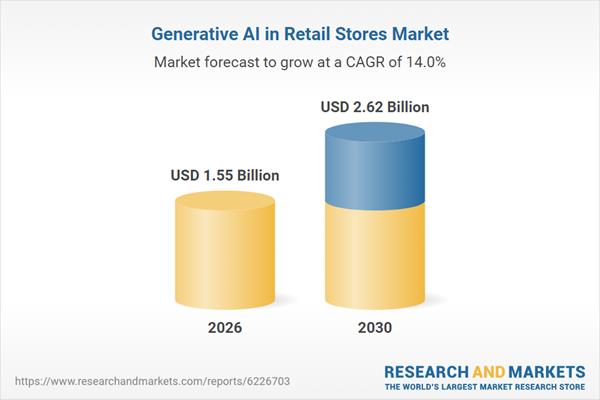

The market for generative AI inside retail stores is no longer a rounding error, but it is not yet the tidal wave the hype cycle promised either. A new market study pegs the segment at 1.55 billion dollars in 2026, up from 1.35 billion in 2025, and projects it will reach 2.62 billion by 2030 at a compound annual growth rate of roughly 14 percent. Those are respectable numbers, but they are notably more grounded than the trillion-dollar figures that circulate when analysts fold in every adjacent category. The value of a narrowly scoped estimate is precisely that it separates deployed, revenue-generating generative AI from the aspirational spend still trapped in strategy decks.

For enterprise buyers, a 14 percent growth rate tells a specific story. This is a market compounding steadily rather than exploding, which is what maturation actually looks like. The froth of 2024, when every retailer announced a generative AI pilot, is giving way to a more disciplined phase where budgets follow use cases that survive contact with a profit and loss statement. The report frames the growth as driven by e-commerce expansion, richer customer data and demand for personalized experiences, all of which are durable rather than speculative. That durability is the point: this is spend that persists after the novelty fades.

The Numbers Behind the Headline

The trajectory is worth stating precisely. From 1.35 billion dollars in 2025 to 1.55 billion in 2026 is roughly a 200 million dollar annual increment, and the path to 2.62 billion by 2030 implies that pace holds and modestly accelerates. A growth rate in the low double digits is neither a bubble nor a disappointment; it is the signature of a technology moving from early adopters into the mainstream of retail operations. The report situates North America as the largest market in 2025, which reflects where the cloud providers, model developers and best-funded retailers are concentrated, and where data infrastructure is most ready to support generative workloads.

The more interesting signal is regional. The study identifies Asia-Pacific as the fastest-growing region, a pattern that mirrors the broader migration of digital commerce toward Asian markets with enormous mobile-first populations and aggressive platform competition. For a multinational retailer, that split has planning implications. The center of gravity for generative AI spend today is North America, but the fastest incremental returns over the forecast window may come from Asia-Pacific deployments. A capital allocation plan anchored solely to headquarters markets risks underfunding the regions where adoption curves are steepest and competitive pressure is most intense.

What Is Pulling Budgets Out of the Lab

The report attributes the growth to a familiar but telling set of drivers: e-commerce expansion, greater availability of customer data, demand for personalization, and advances in the underlying algorithms, alongside cloud-based AI platforms, connected-device integration and augmented reality. Strip away the taxonomy and a pattern emerges. The applications moving from pilot to production are the ones that touch either revenue or a clearly measurable cost. Personalized recommendations, conversational assistants and merchandising analytics justify themselves in conversion and basket size. That is why they are pulling budget while more speculative uses, such as generative store design or synthetic marketing at scale, remain experimental.

The presence of cloud platforms and connected devices in the driver list is a reminder that generative AI in retail is an infrastructure story as much as a model story. The retailers realizing value are the ones that already modernized their data estates, because a language model is only as useful as the product, inventory and customer data it can reach. This is the same lesson visible across the sector this year: platform maturity, not model choice, tends to decide who captures value. The market report quantifies the outcome, but the precondition is unglamorous data engineering that rarely makes the announcement.

The Vendor Land Grab

The vendor list the report names reads like a map of where the fight is being waged. The hyperscalers appear in force, with Google, Microsoft and Amazon Web Services, alongside chip and systems players such as NVIDIA and Intel, and enterprise software incumbents including IBM, Oracle, Salesforce and Adobe. Then come the retail specialists: Zebra Technologies, Blue Yonder, RetailNext, Algolia, Everseen and Klevu, among others. The breadth is the story. Generative AI in retail is not a category any single vendor owns; it is a stack where infrastructure, models, applications and point solutions are being assembled, often uneasily, into something a retailer can actually run.

For a CTO, that fragmentation is both an opportunity and a warning. The opportunity is choice and competitive pricing across every layer. The warning is integration risk, because a generative capability stitched together from a hyperscaler model, a specialist search engine and an incumbent commerce platform inherits the seams between them. The vendors with the strongest position are those that can credibly span multiple layers, which is why the cloud providers loom so large. Buyers should be wary of assembling a best-of-breed stack whose total cost of integration and maintenance quietly exceeds the value the generative features deliver.

Where the Growth Is Moving

The forecast implicitly charts a migration from back office to storefront. Early generative AI budgets in retail skewed toward internal productivity, content generation, code assistance and analyst support, because those uses were low-risk and easy to justify. The drivers the report emphasizes, personalization, conversational commerce and customer data, point toward customer-facing deployment, where the technology is riskier but the revenue upside is larger. That shift is the real narrative inside the numbers: the spend is moving toward the parts of the business where a generative system can lift sales, and therefore toward the parts where its errors are most visible to shoppers.

This is where the market steady growth rate and its risk profile intersect. Customer-facing generative AI raises the stakes on accuracy, brand voice and trust, which is why adoption compounds at 14 percent rather than doubling annually. Retailers are, sensibly, pacing themselves. They are moving generative capabilities toward the storefront only as fast as they can guarantee the outputs will not embarrass the brand or misinform a customer. The forecast, read carefully, describes an industry that wants the upside of conversational commerce but is unwilling to wreck customer trust to get there quickly.

Reading the Forecast With a Skeptical Eye

A market-sizing report is a useful compass, not a map, and executives should treat it accordingly. Definitions drive everything in these studies, and a narrow scope that excludes adjacent spend on data infrastructure, integration and change management will understate what a generative program actually costs a retailer. The 1.55 billion dollar figure measures a defined slice of technology spend, not the full investment required to deploy it responsibly. Read as a directional signal, it is valuable. Read as a budget, it is misleading, because the true cost of putting generative AI in front of customers lives largely outside the category the report measures.

Our takeaway is that the number matters less than the shape it describes. Steady double-digit growth, a vendor field spanning every layer of the stack, and a clear migration toward customer-facing use cases together describe a technology settling into the operational core of retail. The exuberant phase is ending and the accountable phase is beginning. For enterprise leaders, that is the more useful frame than any single dollar figure: generative AI in retail is now a line item to be managed and measured, not a moonshot to be announced, and the discipline of the next four years will separate the retailers who profit from it from those who merely funded it.