A Reckoning Priced Into the Market

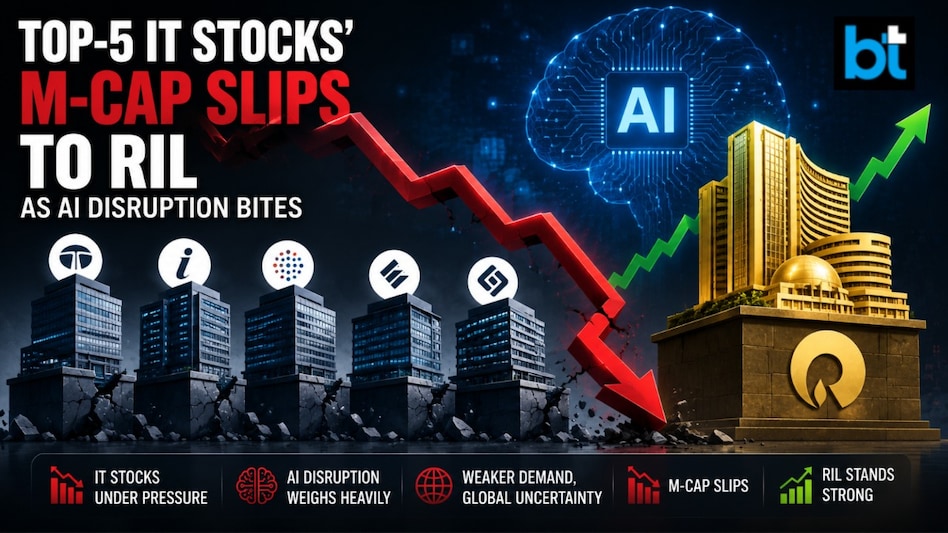

The combined market capitalisation of India's top five IT services firms, Tata Consultancy Services, Infosys, Wipro, HCL Technologies and Tech Mahindra, has collapsed roughly 46 percent to about Rs 18.15 lakh crore, down from a record Rs 33.71 lakh crore in August 2024. As of 4 July 2026, that pooled value now sits level with a single company, Reliance Industries, whose own Rs 17.65 lakh crore reflects a comparatively mild 16.7 percent correction. For an industry that spent two decades as the reliable compounding engine of Indian equities, the symbolism is hard to miss.

We read this less as a cyclical dip and more as the market repricing a business model. Investors are no longer paying premium multiples for headcount-linked revenue when the headcount itself is the variable AI is designed to compress. The question hanging over every earnings call is no longer whether demand will recover, but whether the unit economics that made these firms great still hold once generative tooling sits inside the delivery pipeline.

What AI Deflation Actually Means

The phrase doing the rounds among analysts is AI deflation, and it is worth unpacking because it is not the same as weak demand. JP Morgan, which flagged the dynamic, warns that AI deflation is still only in its second year and could create further headwinds over the next two years. The mechanism is straightforward: as generative tooling automates code, testing and support work, the same scope of a client engagement now requires fewer billable hours, and clients expect to pay accordingly.

That produces a paradox the sector has not faced before. A vendor can deliver more output, win the same logos, and still watch revenue per contract shrink. For firms whose growth was historically a function of adding engineers, the lever that once drove the top line has become the thing eroding it. JP Morgan's sequential second-quarter estimates capture the squeeze: Infosys at 1 to 2.5 percent, HCLTech at 1 to 3.5 percent, and Wipro at negative 2 to flat.

The Accenture Warning Shot

The proximate trigger for the latest leg down came from outside India. Accenture trimmed its fiscal 2026 revenue guidance to 3 to 4 percent from 3 to 5 percent, citing a roughly 100 million dollar hit tied to the Middle East conflict and about 400 million dollars of EMEA drag from slower enterprise decision-making. Because Accenture is treated as a bellwether for global services spending, its caution reverberated straight through Mumbai, sending Infosys shares to a five-year low and TCS toward a six-year trough.

We would caution against reading the Accenture number purely as geopolitics. The more durable signal is slower decision-making, code for enterprises pausing large transformation programmes while they figure out what agentic AI does to their own operating models. Buyers are not cancelling digital transformation, they are hesitating, and hesitation is expensive for vendors whose bench is already staffed for a recovery that keeps sliding right.

The Linear-Growth Model Under Pressure

For a generation, the Indian IT thesis was elegantly linear: win a deal, staff it with engineers, bill for their time, repeat at scale. That model rewarded pyramid structures, aggressive fresher hiring, and utilisation discipline. It did not reward, and in some ways actively discouraged, the kind of productivity that lets a firm deliver a project with a fraction of the people.

Generative AI inverts that incentive overnight. The vendors now have to sell clients on doing more with less, which is precisely the opposite of a revenue model built on billing hours. We think the firms that navigate this will be the ones willing to cannibalise their own labour arbitrage before a competitor or a client platform does it for them. The market's brutal repricing is, in effect, a demand that they prove they can.

What CIOs Should Read Into This

For the CIOs and CTOs who buy these services, the selloff is not schadenfreude material, it is a planning input. If your strategic partner's economics are under this much strain, you need to understand how they intend to keep delivery quality and talent depth intact while their margins compress. Ask pointed questions about how AI-driven productivity gains will be shared, because the vendor that absorbs all of them quietly is not a partner, it is a counterparty.

There is opportunity here too. Buyers with leverage can renegotiate toward outcome-based and productivity-linked pricing, capturing part of the deflation the vendors are experiencing. The enterprises that treat this moment as a chance to restructure their services contracts, rather than simply riding legacy time-and-materials deals, will come out of it paying less for measurably more.

Not Only an India Story

It would be a mistake to file this under emerging-market volatility. The same forces are pressing on Accenture, Cognizant, Capgemini and every services house whose revenue is a function of billable effort. The Indian majors simply carry the largest, most labour-intensive delivery engines, which makes them the clearest place to watch the deflation play out in real time. When JP Morgan warns of two more years of headwinds, it is describing an industry-wide repricing, not a regional wobble.

The difference is one of exposure, not direction. Firms with more software, more platform revenue and more onshore consulting will feel the compression later and less acutely. Pure labour-arbitrage players will feel it first and hardest. For enterprise buyers, that is the useful lens: judge each partner by how much of its value comes from people you can now partly automate, versus intellectual property you still cannot.

Rebuilding on Outcomes, Not Headcount

The path forward for the sector is not mysterious, only difficult. It runs through outcome-based commercial models, proprietary AI platforms that create differentiation beyond raw labour, and a genuine reskilling of the pyramid toward higher-value architecture and governance work. The firms that get there will look less like staffing agencies and more like software companies with services attached, and they will price accordingly.

We do not expect that transition to be smooth, and the market clearly agrees. A 46 percent drawdown is the sound of investors demanding proof rather than promises. For an industry that helped digitise the rest of the world, the harder assignment has finally arrived: digitising, and de-risking, itself, before its own clients and the platforms they run learn to do without it.